.svg)

20% Tax On Your Savings? Wrong—Here’s The Truth

“Do they really have the best interest of Filipinos in mind when they pass laws like this?”

This is a question that now echoes across lunch tables, online forums, and family group chats. Netizens most especially show a familiar mix of confusion, frustration, and resignation caused by another sweeping tax policy that has been passed—the commotion is made even worse by the blatant spread of misinformation, fueled by misleading news headlines and biased framing.

What They Got Wrong

We’re talking about the very controversial Capital Markets Efficiency Promotion Act (CMEPA)—which faulty media announcements made a lot of people think that the government would mandatorily impose a 20% principal tax deduction on all forms of savings and passive incomes.

As it turns out, it’s not the principal, but only the interest generated from the principal amount that’s going to be taxed. Surely, it’s still enough to raise an eyebrow, but it’s important to get all the facts straight.

We get it, but here’s what you need to know.

What It Actually Means—The Legal Mechanics Behind CMEPA

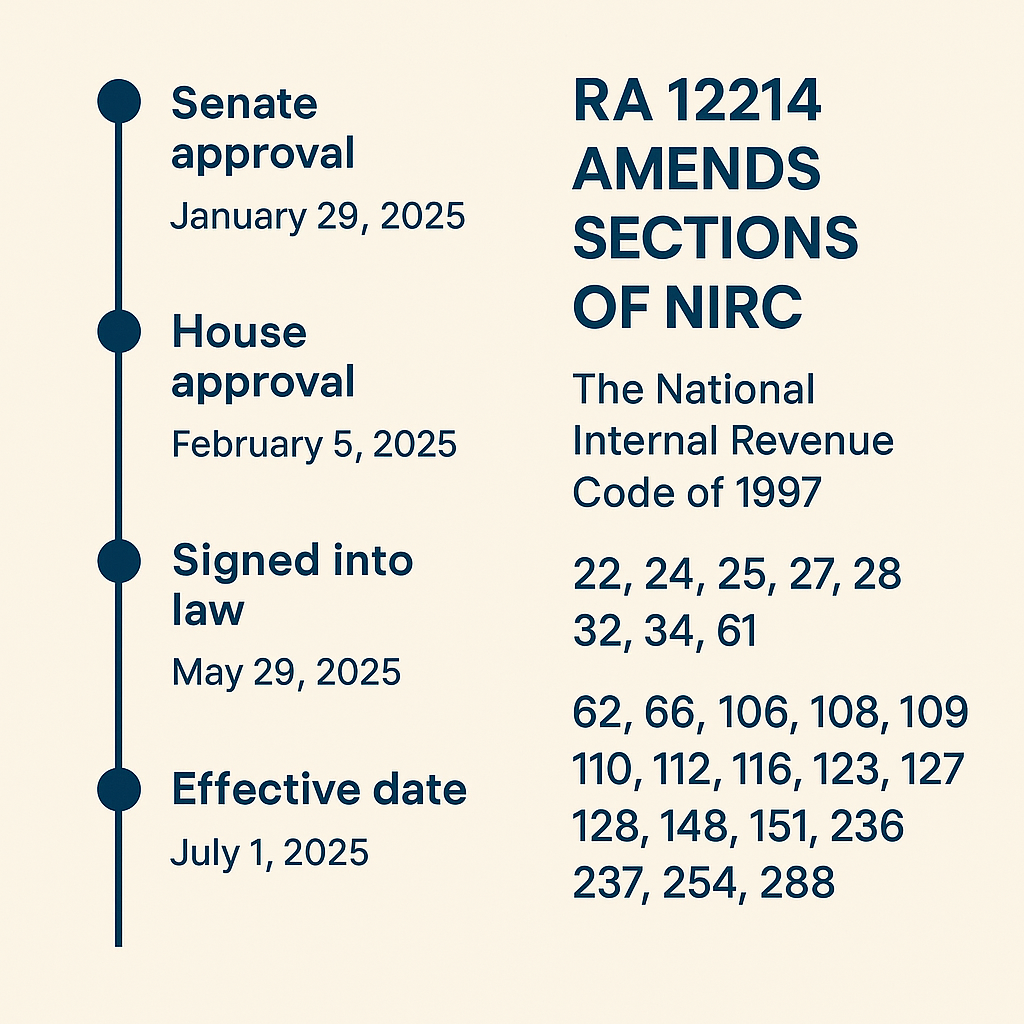

To clear the misconceptions, Republic Act No. 12214, known as the Capital Markets Efficiency Promotion Act (CMEPA), is not merely a reform bill—it is a new law enacted on May 29, 2025, amending several sections of the National Internal Revenue Code of 1997 (RA 8424). It updates already existing tax-code provisions, and was signed into law as a new statute, not simply a revision of prior legislation.

The law took effect starting July 1, 2025, following its official publication, and includes sweeping policy changes like standardizing withholding taxes, cutting trading costs, and expanding PERA provisions.

Before CMEPA:

- LONG TERM peso time deposits held exactly 5 years or longer were tax-exempted

- SHORTER TERM peso time deposits were taxed, but on a graduated scale:

- 20% for less than 3 years

- 12% for less than 4 years

- 5% for less than 5 years

- 15% for foreign currency time deposits for residents and corporations

After CMEPA:

- 20% tax on ALL short or long-term time deposits, peso or foreign currency as long as made by a certified Filipino resident or corporation

- No exemptions, no gradual rates.

To reiterate, tax is applicable NOT on principal amount.

Nevertheless, the 20% tax on deposit interest is in fact just one part of RA 12214’s wider overhaul of financial taxation. It’s more than what only meets the eye. It seeks to restructure how financial income is taxed in the Philippines—from stock trades to mutual funds to retirement accounts.

The upside:

- Stock Market Investors

The stock transaction tax is reduced from 0.6% to 0.1%, encouraging more participation in equities.

- Mutual Fund Holders

Documentary stamp tax is removed on collective investment schemes, lowering investment costs.

- PERA Savers

Expanded incentives now allow higher contributions and tax-free growth for retirement savings.

- Private Shareholders

Capital gains on unlisted shares are now taxed at 15% on net gains—a fairer shift from the previous 6% on gross selling price.

Therefore, the amendment in its core intends to benefit and give investors and shareholders a better fighting chance in the market—for a price. The question now shifts from, ‘Is the government discouraging people to save?’ to ‘Is the government pushing people to be less passive with their money?’

The majority didn’t see this coming, it indeed caught a lot of people off guard. It is why the clamour coming even for those who are sufficiently informed and well-versed about the law is understandable—with some people arguing that it further worsen inequity among social classes; putting more burden downwards.

The Weight of Amendment—Listening To Local Sentiments

Let’s talk about what this looks like in real life.

Imagine Ana, a single parent working two jobs, who scrapes together ₱200,000 and places it in a 5-year time deposit—her hardearned peace of mind. Under the old law, her savings were exempt from tax after long-term maturity. Now, with CMEPA in effect, even after 5 years, 20% of generated interest from her time deposit account will automatically be withheld from her earnings. Assuming that her time deposit account is generous enough to give 6% interest annually, that means tax amounting to a total of ₱12,000. So, instead of around ₱60,000 total interest earned, she would get ₱48,000 net interest throughout the 5 year time period. Would the amount still be a bother if it means contributing to the betterment of the nation?

Or Mang Tonyo, a retired jeepney driver who trusted the bank with his meager retirement fund. He may not own stocks. He doesn’t trade crypto. His long term deposit interest was all he could count on—having it taxed gives his money a slimmer chance to win against inflation.

This is the hidden cruelty of flat taxation: it assumes equality where inequality is the norm. It reduces fairness to simplicity—and simplicity, in this case, means taking more from those who have less.

The Promise vs. The Pain—CMEPA’s Good Intentions, Questioned

To be fair, CMEPA was not crafted in bad faith. Its architects point to global standards, capital market growth, and revenue gains. The Department of Finance projects ₱25 billion in additional revenue by 2030, citing simplified tax structures and stronger investor confidence.

But let’s ask: confidence for whom?

Indeed, institutional investors may benefit from reduced trading frictions and tax predictability, but ordinary citizens face more reasons to distrust the system. When the government taxes a wage earner’s meager deposit income at 20%, but offers retirement perks to equity holders and bond investors, is reform or unfair reallocation.

Reform should uplift, not flatten. And tax efficiency shouldn’t come at the cost of financial inclusion. The promise of capital markets is meaningless if Filipinos feel punished for saving.

On top of it all, let’s not forget to address the looming elephant in the room. What makes people indignant and mad about this may not be all the taxing itself, but how pervasive yet obscure how tax is being used for the benefit of the Filipinos—especially hardworking taxpayers.

Rural and urban transportation and traffic can be so inconvenient and time consuming that it’s not even a hyperbole to say that it drains a good portion of your lifeline; urban planning and drainage systems are sight for vertigo, not to mention government websites and services being a bunch of barely functional relics with ugly UI. Would new tax laws pave the way for a better system? Regardless, what all Filipinos could do is to keep on working hard and hope for the best.

.svg) SHARE TO FACEBOOK

SHARE TO FACEBOOK SHARE TO TWITTER/X

SHARE TO TWITTER/X SHARE TO LINKEDIN

SHARE TO LINKEDIN SEND TO MAIL

SEND TO MAIL

.svg)

.svg)